Storm Roof Damage in Louisiana: The First-24-Hour Playbook

Quick Answer: After a Louisiana storm damages your roof, the first 24 hours decide how the next six months go. Document everything before you touch anything. Contact your insurance carrier the same day. Call a local roofer for a free inspection before the carrier’s adjuster arrives. Do not climb the roof yourself. Do not let a door-knocking storm chaser pressure you into signing anything. The decisions you make today will determine if your claim pays out in full or leaves you covering the gap.

TLDR:

- Document damage immediately: photos, videos, dated notes. Cover everything before you move it.

- Call your insurance carrier the same day to open the claim. Get the claim number in writing.

- Get a free roof inspection from a local roofer BEFORE the carrier’s adjuster arrives. Your roofer should attend the adjuster meeting.

- Tarp + cover any active leaks to prevent further damage. Save receipts. Carriers reimburse reasonable mitigation costs.

- Do NOT sign anything from a door-knocking storm chaser, especially Assignment of Benefits (AOB) language. Read everything twice.

- Save every email, voicemail, and adjuster note. Build the paper trail from day one.

- Know your deductible math before the call. Louisiana hurricane deductibles are percentage-based and much larger than your annual deductible.

- Replacement Cost Value (RCV) and Actual Cash Value (ACV) are not the same thing. The settlement structure matters more than the headline number.

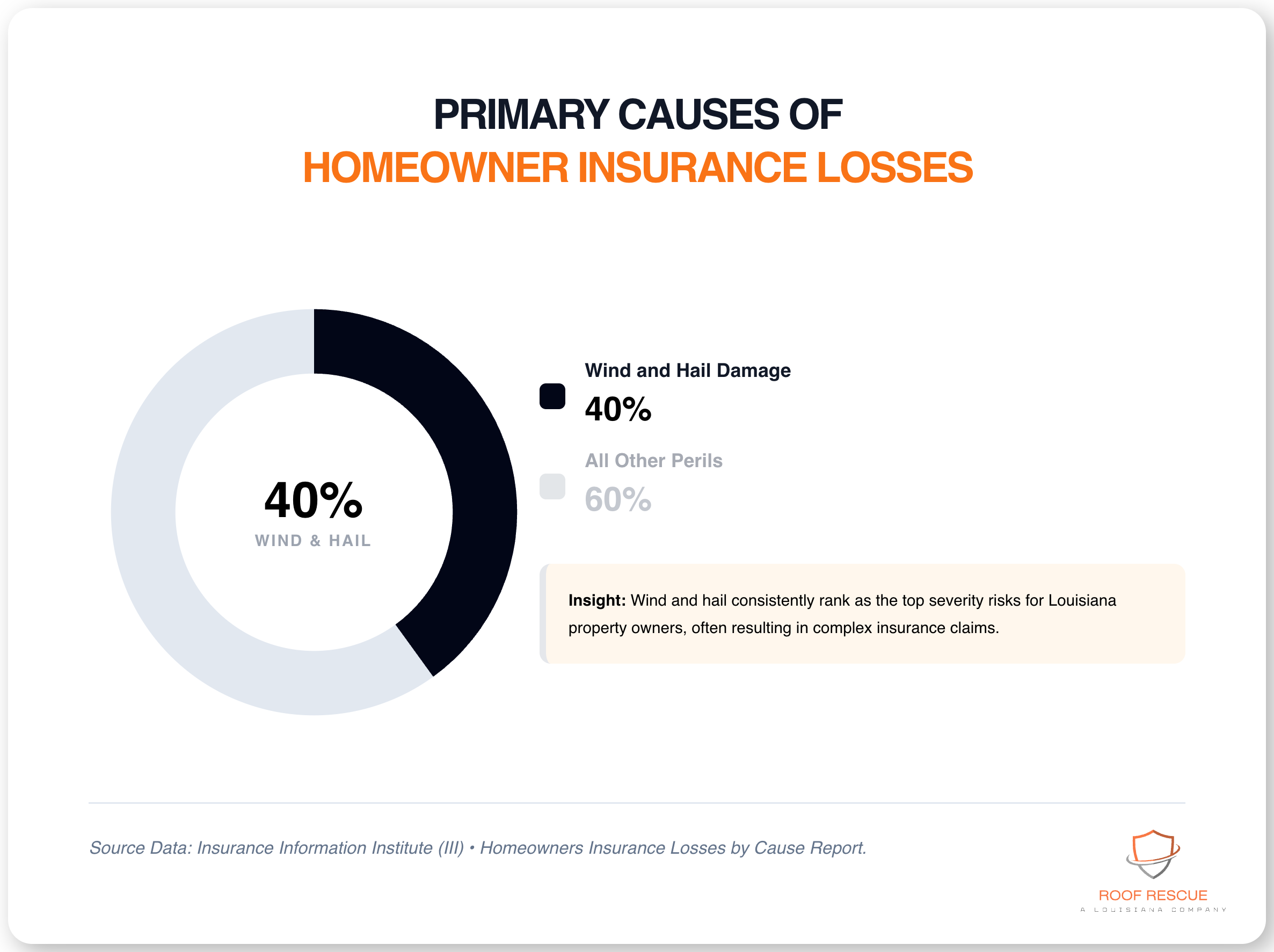

Louisiana storm season runs from spring severe thunderstorms through November-end hurricane closure. Between hail, straight-line winds, and named storms tracked by the NOAA National Hurricane Center, most homeowners in the Baton Rouge metro will deal with roof damage at some point. The frustrating part is not the damage itself. It is about how quickly the timeline moves once damage occurs and how many decisions homeowners are asked to make in the first 24 hours while they are still rattled.

This guide is the playbook we walk our customers through after a storm. It works for homeowners in Zachary, Denham Springs, Prairieville, Hammond, Gonzales, Mandeville, and anywhere else in our service area. The principles are the same statewide.

Roof damage after a Louisiana storm? Call or text 225-369-3601 for a free roof inspection. We respond fast during storm seasons, and we know how to document damage in the language insurance carriers actually accept.

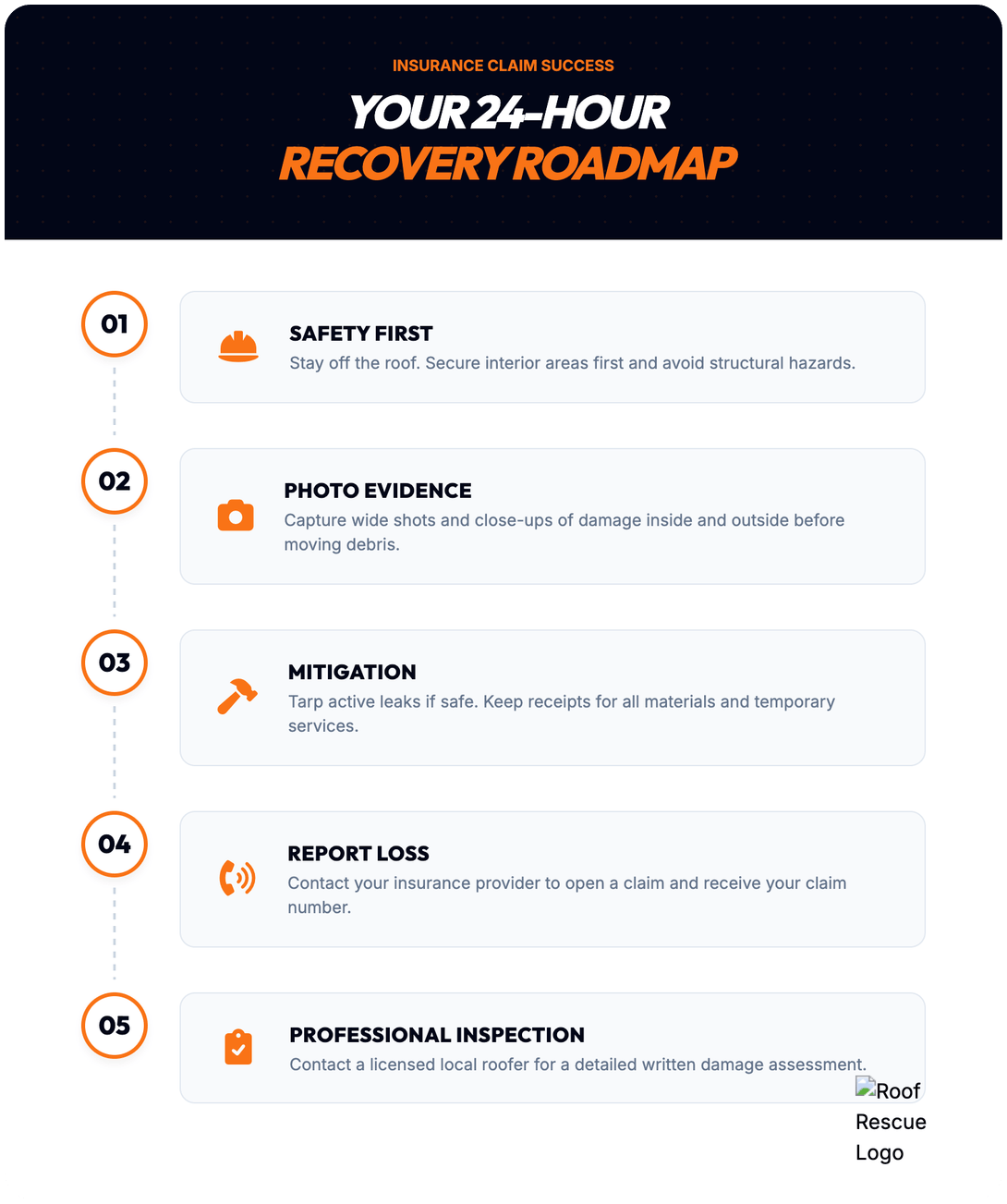

Hour 0 to 4: Safety First, Documentation Second

Before anything else: do not climb on the roof. Wet shingles, hidden structural damage, and downed power lines kill homeowners every storm season. The carrier does not need you to inspect the roof yourself. Your roofer does that, with safety equipment and the experience to know what is structurally sound.

From the ground, here is what you should do in the first four hours.

Document the damage from the outside

Walk the perimeter of the house. Take photos and video with your phone of:

- Every angle of the roof from ground level

- Visible missing or lifted shingles

- Debris on the roof, in the gutters, or in the yard

- Tree limbs or fallen objects that hit the structure

- Any siding, window, or fascia damage adjacent to the roof

- The date and time visible on your phone or a piece of paper in the photo

If you can safely use a drone or get a second-story window view, do that too. Time-stamped video is even better than photos for showing the scope of damage.

Document the damage from the inside.

Walk through every room of the house with the lights on. Look for:

- Water stains on ceilings (even small brown rings matter)

- Bulging paint or sheetrock

- Dripping water (catch it in a bucket, photograph the bucket + drip pattern)

- Damp insulation in the attic (carefully; do not enter the attic if there is any chance of structural compromise)

- Water on floors, especially near exterior walls

- Damaged personal property from leaks

Photograph everything. Even damage you think might be unrelated to the storm. Adjusters argue the scope every day, and your contemporaneous photos are the strongest evidence you have.

Cover anything actively leaking.

If water is coming in actively, your job is to mitigate further damage. Move furniture and electronics away. Place buckets or tarps. Throw a plastic tarp over the affected area if you can do so SAFELY from the inside (running a tarp from inside the attic up through a damaged spot is sometimes possible). Do not climb the roof for this. If the leak is severe enough to need a roof tarp, that is what your roofer does.

Carriers reimburse reasonable mitigation costs under the Duty After Loss clause in most Louisiana homeowner policies. Save every receipt. Tarps, buckets, fans, and dehumidifiers are all reimbursable if documented.

Hours 4 to 12: The First Two Phone Calls

The order matters here. Call your insurance carrier first, then call a local roofer.

Call your insurance carrier.

Open the claim the same day if at all possible. The Insurance Information Institute’s homeowners claim process guide notes that carriers track the timing between damage and first notice of loss, and a same-day or next-day notice removes one argument from the claim file later.

When you call:

- Get the claim number in writing (email confirmation, screenshot of the claims portal)

- Note the time you called and the name of the rep you spoke with

- Ask when the adjuster will be assigned and when you can expect contact

- Do NOT estimate the scope of damage on the phone (“just a few shingles” can come back to haunt you). Stick to facts (“the storm hit at X time on Y date, there is visible damage and active water entry”)

- Ask if the policy has a separate hurricane or wind/hail deductible. Louisiana policies often do (see below).

Some carriers will try to send their own preferred roofer or have you use a claim concierge service. You are not required to use either. You have the right to choose your own roofer.

Call your roofer

Get a free inspection scheduled as soon as possible. The reason is timing: the carrier will send an adjuster, and you want your roofer’s documentation in hand BEFORE the adjuster shows up. Better yet, you want your roofer to be present during the adjuster’s inspection.

When you call us at Roof Rescue, here is what happens:

- We respond same-day or next-day for storm damage (faster in the immediate aftermath of named storms)

- We do a full roof inspection, including ground photos, a drone if conditions allow, and an attic check

- We document damage in the format carriers actually accept (with specifics on shingle count, decking exposure, ventilation compromise, gutter and flashing condition, code-upgrade triggers)

- We give you a written scope and estimate. This is YOUR document. You decide what to do with it.

- If you ask us to, we coordinate with your adjuster. We have done this with every major Louisiana carrier.

Why timing matters: Adjusters work fast. Their job is to settle the claim at the lowest defensible amount. Your job is to make sure the documentation tells the full story. A roofer’s inspection report from BEFORE the adjuster’s visit gives you leverage. It also gives your adjuster a starting point that reflects reality, which often saves time for both sides.

Hours 12 to 24: The Mistakes That Cost Claims

Most claims that pay poorly do so because of mistakes the homeowner made in the first 24 hours. These are the most common.

Mistake 1: Signing an Assignment of Benefits to a door-knocking storm chaser

After major storms, out-of-state contractors fan out across affected neighborhoods. They knock on doors offering “free roof replacement” or “we handle everything with insurance, you pay nothing.” They ask you to sign an Assignment of Benefits (AOB) form. The FTC’s consumer guide to hiring a contractor covers the warning signs to watch for, including door-to-door pressure tactics that spike in the days after major storms.

An AOB transfers your right to negotiate with the carrier directly to the contractor. After you sign, you are out of the loop. The contractor and the carrier negotiate. The contractor gets paid first, regardless of how the work turns out. If something goes wrong, you have very little recourse.

Louisiana has tightened some AOB rules, but the form still exists in practice. The simple rule: do not sign anything from a contractor who showed up uninvited at your door after a storm. A legitimate local roofer does not need an AOB. They will work with your claim and bill you directly per the carrier’s settlement.

Mistake 2: Letting the carrier’s preferred contractor do the work without independent review

Carriers maintain networks of “preferred” roofers who agreed to certain pricing and scope norms. The carrier saves money. The question of how complete a scope you actually get is a separate matter.

You can absolutely use a preferred contractor if you want to. But get a second opinion from an independent local roofer first. The estimates may differ in important ways. Scope of replacement vs. repair, decking exposure, and code upgrades. You should understand what is (and isn’t) in the carrier’s preferred scope before agreeing.

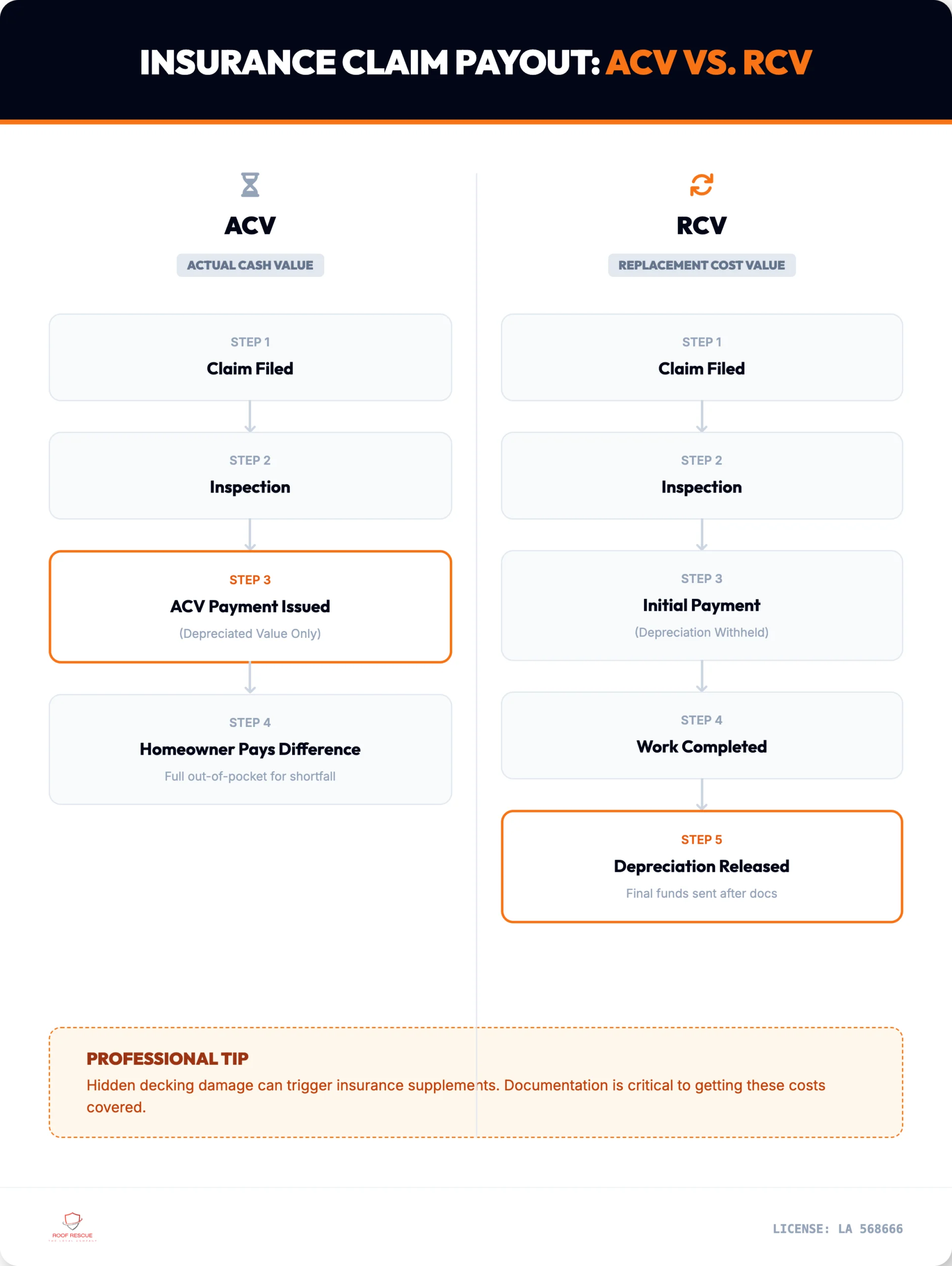

Mistake 3: Accepting the first settlement check without understanding RCV vs ACV

Most modern Louisiana homeowner policies pay claims on a Replacement Cost Value (RCV) basis. The carrier sends a first check for Actual Cash Value (ACV), which is RCV minus depreciation. The Insurance Information Institute’s breakdown of Actual Cash Value covers exactly how depreciation gets calculated for claim purposes. Once you complete the work and submit final invoices, you can recover the depreciation amount with a supplemental claim.

If you cash the first check and walk away, you leave the depreciation on the table. For a roof claim, that depreciation amount can be substantial. The Triple-I guide to depreciation on homeowners’ claims explains the math and what triggers recovery.

The settlement process is normal. The mistake is thinking the first check is the whole claim. It is not.

Mistake 4: Throwing away damaged materials before the adjuster sees them

Even if a shingle is in three pieces on the ground, do not throw it away. Bag it, label it with the storm date, and keep it until the claim closes. Carriers occasionally argue about hail size or wind direction, and the actual damaged materials are your strongest evidence.

Mistake 5: Talking yourself into “it can wait.”

After the rush of the first few hours, the temptation is to put off the calls. The damage looks contained. Maybe the leak stopped. Maybe the claim feels like more hassle than it is worth.

Storm damage compounds. Water that enters the wall cavity rots the framing. Dampened insulation grows mold. Compromised flashing leaks more in the next storm. Every week of delay shifts the homeowner from “covered claim” to “long-term water damage.” The long-term damage often is NOT covered, on the carrier’s argument that you failed your duty to mitigate.

The 24-hour window is real. After 72 hours, claim outcomes get noticeably worse.

What Louisiana Homeowners Should Know About Their Policy

Before you call your carrier, it is worth knowing a few specifics about Louisiana homeowner insurance that catch homeowners off guard.

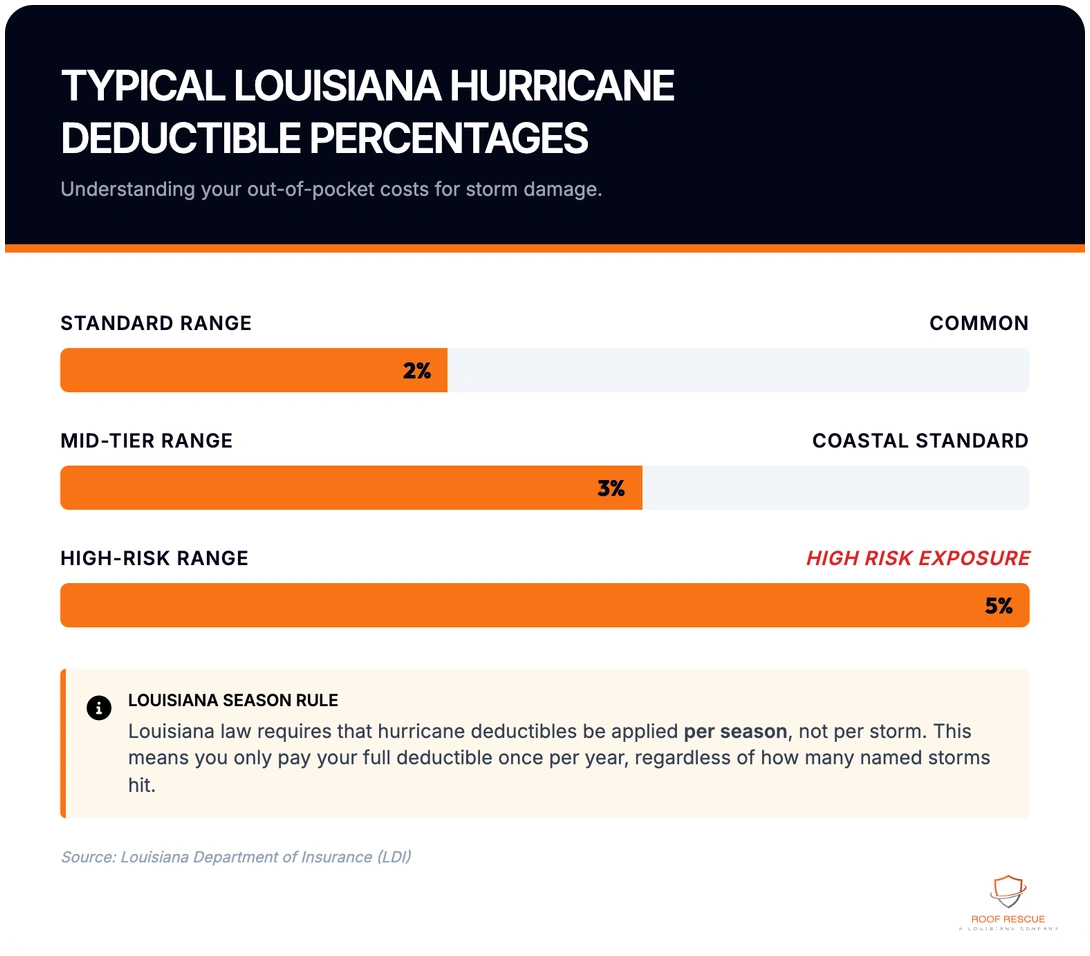

Hurricane deductibles are percentages, not flat amounts.

Most Louisiana policies have a separate deductible for named storms. Instead of your usual flat-dollar deductible (often $1,000 or $2,500), the named-storm deductible is a percentage of the dwelling coverage. Two percent is common. Five percent is not unusual in areas with coastal exposure. The Insurance Information Institute’s deductible explainer and the Louisiana Department of Insurance consumer resources both cover how named-storm deductibles are structured.

On a home insured for $400,000 dwelling coverage at a 2% hurricane deductible, the deductible is $8,000. At 5%, it is $20,000. That is the amount you pay before insurance pays anything on a hurricane claim.

Know your deductible before the call. The carrier’s first question is often if the damage exceeds the deductible. If you have not done the math, you cannot answer with informed confidence.

ACV vs RCV materially changes your math

Replacement Cost Value reflects the actual cost to replace the roof with materials of like kind and quality. Actual Cash Value equals RCV minus depreciation for the roof’s age and condition.

On a 15-year-old asphalt roof, the ACV settlement might be 40-60% of the replacement cost. The remaining 40-60% comes through the supplemental claim AFTER work is complete. Many homeowners do not realize this and feel underpaid on the first check.

The supplemental process is normal, but it requires you actually to complete the work and submit final invoices. Walking away after the ACV check forfeits the depreciation recovery.

Code upgrade coverage (Ordinance or Law) is separate.

Louisiana adopted updated roofing codes (including fortified-roof requirements in some jurisdictions) that often require upgrades beyond what was installed when the original roof went on. The IBHS Fortified Home program, recognized by Louisiana for insurance discounts, sets the standard for these upgrades. Carriers usually offer a separate “Ordinance or Law” coverage that pays for code-required upgrades.

If your policy has it (most do, at 10% or 25% of dwelling coverage), make sure the carrier applies it to the claim. We have seen claims where the homeowner did not know they had Ordinance or Law coverage, and the carrier did not volunteer it.

Matching statute issues for partial roof claims

Louisiana has a “matching statute” that requires carriers to pay for materials that match existing undamaged materials in some circumstances. The practical question often arises when one side of a roof is damaged, and the carrier wants to pay only for that side. Matching the rest can be impossible. Your existing shingles are 12 years weathered, and the new ones are not.

The statute does not guarantee a full replacement. It depends on the policy language, the carrier, and what is reasonable. But it is a real argument when partial replacement would leave the roof aesthetically or functionally mismatched. Make sure your roofer raises this in the adjuster meeting if it applies.

Day 2 Onward: What Happens Next

If you got through the first 24 hours with documentation in hand, the carrier notified, and a local roofer engaged, then the next few weeks follow a known pattern.

| Stage | Typical timing | What to expect |

|---|---|---|

| Adjuster contact | 24-72 hours after claim opening | Phone call to schedule the inspection visit. Get this on the calendar fast. |

| Adjuster inspection | 3-7 days after first contact | The adjuster visits, measures, photographs. Your roofer should be present. |

| First settlement letter | 7-21 days after inspection | Initial determination, with the ACV check (if RCV policy) or the full payment (if ACV-only policy) |

| Roofer scheduling | After settlement is reviewed | Schedule the work. Communicate any scope disagreements BEFORE the work starts. |

| Supplemental claims | During or after the work | If the work uncovers additional damage (rotted decking, etc.) or code upgrades (ventilation, flashing), file a supplemental claim while it’s documentable. |

| Final invoices + RCV recovery | After work completes | Submit final invoices to carrier for depreciation recovery. Usually paid within 30 days of receipt. |

| Claim closes | Varies | Some claims close in 4-6 weeks. Hurricane claims can take 6-12 months in heavy-loss periods. |

The timing matters because each stage has a deadline (most policies require the supplemental claim within 12-24 months of the date of loss). Track your dates. Most carriers have a portal where you can see them, or your roofer can help you keep a timeline.

Considering a roof claim from a recent Louisiana storm? Roof Rescue walks every customer through this process. We do not charge for the inspection or the adjuster meeting. We charge for the actual roofing work, billed against the carrier’s settlement.

Call or text 225-369-3601, or request a free roof inspection to have us walk your property.

Common Questions Louisiana Homeowners Ask After a Storm

These are the questions we get most often in the first 24 hours after damage. If something is happening at your house right now and you need a faster answer, call us.

How do I know if my roof damage is from this specific storm or pre-existing?

This is one of the most common claim arguments. The honest answer is that some damage is unambiguous (a tree limb on the roof, fresh hail bruising) and some is harder to date. A roofer with experience documenting Louisiana storm damage can usually point to specific characteristics that align with the storm date: the orientation of impact patterns, fresh tear lines, and consistent damage across exposed slopes. Your contemporaneous photos from the day of the storm are critical here. So is your roofer’s documentation.

Should I file a claim if my deductible is high?

Do the math first. If your hurricane deductible is $10,000 and the damage looks like a few missing shingles, the claim is likely not worth filing. If the damage looks like a full replacement (which can run $15,000 to $40,000+ in Louisiana, depending on size and material), the claim is clearly worth filing, even with a $10,000 deductible. The free inspection from a local roofer gives you a realistic scope of the damage so you can make an informed decision.

Can I get a roof replaced with no out-of-pocket cost beyond my deductible?

Often, yes, when the carrier settlement covers the replacement scope your roofer recommends. The deductible is your share, and the rest comes from insurance. The cases where homeowners pay more than the deductible usually involve upgrades the homeowner chose (premium materials, additional code-recommended upgrades not covered), gaps between the carrier’s scope and the work that actually needs to be done, or scope disputes that did not get resolved before the work started.

What if the carrier denies my claim?

Denials happen, especially on partial claims or older roofs. Common reasons: insufficient documentation, the carrier’s adjuster determining the damage was pre-existing, or the damage not exceeding the deductible. The next step is usually to request a re-inspection (often with a different adjuster), bring your roofer’s documentation into the conversation, and, in cases of bad-faith denial, consider involving a public adjuster or attorney. Do not give up after the first denial. Many claims initially denied are paid after re-inspection with proper documentation.

Do I have to use the carrier’s preferred contractor?

No. You have the right to choose your own roofer. The carrier may push for a preferred contractor, sometimes by offering faster settlement or implied guarantees. You are still free to choose otherwise. Get at least one independent estimate before deciding.

What if a contractor offers to “waive my deductible”?

Walk away. Waiving the deductible is illegal in most cases (it constitutes insurance fraud), and contractors who offer it signal that they are willing to break the rules. That usually means they will cut corners in other places, too. Legitimate roofers collect your deductible. The carrier expects you to pay it. Anyone telling you otherwise is a red flag.

How long do I have to file the claim?

Most Louisiana homeowner policies require notice of loss “as soon as practicable” or within a specific window (often 30 days for water damage, longer for some other categories). For hurricane claims, faster is always better. By the time you are weighing your options, the answer is almost always yes. File the claim, then decide if you will pursue it based on the inspection and the deductible math.

Roof damaged in a recent Louisiana storm? Get a free roof inspection from a local roofer who knows the claim process.

Roof Rescue is a roofing company in Zachary, Louisiana, serving the Baton Rouge metro and greater Louisiana. We are an Owens Corning Preferred Contractor. Founder Chase Lord came from the fire department before founding Roof Rescue, and that emergency-response background shapes how we respond after storms.

Call or text 225-369-3601 for same-day storm response, or schedule a free roof inspection online.